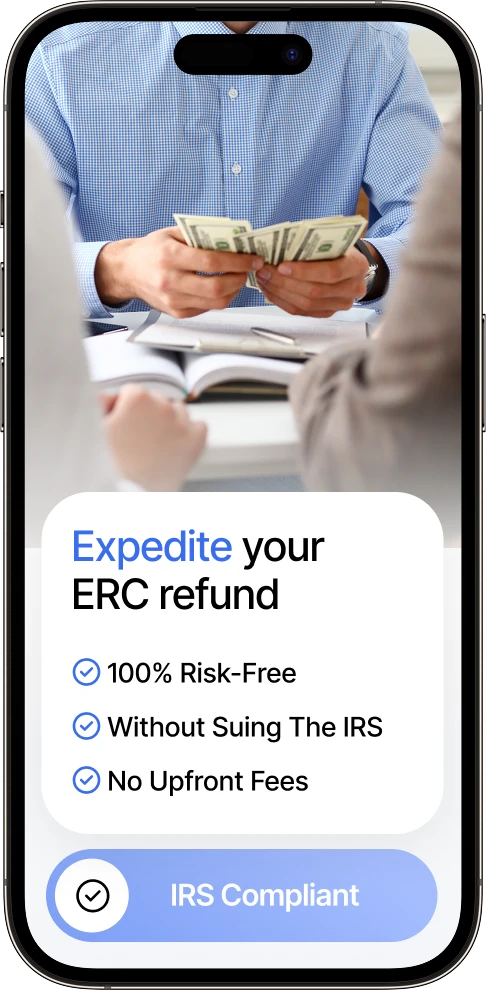

No Risky Lawsuits

No Upfront Fees

No Waiting Years for the IRS!

Over 1.5M businesses are still waiting — don’t risk losing your refund. Expedite your Claim now and get your IRS checks fast

The Longer You Wait, the Higher the Risk

No Risky Lawsuits

No Upfront Fees

No Waiting Years for the IRS!

First Come,

First Serve!

ERC Funds Remaining

$150B ![]()

ERC $ left for applicants

40% ![]()

Complete application

in just 15 min ![]()

If your business filed an ERC claim and is still waiting, you’re not alone.

With over 1.5 million ERC claims stuck in the IRS backlog—still unassigned to an agent—and funds running out fast, businesses who don’t expedite could be waiting years—if they get a check at all.

Сlock is ticking

The Problem?

Take ERC refund control

We’re the only tax firm that can expedite your claim without suing the IRS—secure your ERC refund before it’s too late!

You've waited long enough—here’s how to take control and fast-track your ERC refund today

Expedite your claim

we are trusted

The Solution! — Expedite Your ERC Refund With IRSplus

No matter who originally filed your claim, we can step in and expedite it — without needing anything from them.

Don’t let delays cost you your refund!

Expedite your claim

Why Businesses Trust

IRSplus — The Only Proven Solution to the ERC Backlog

Businesses Trust us

You’ve waited long enough — here’s how to take control and fast-track your ERC refund today!

We Have You Covered

Hospitality

$3M+

Retail

$3.6M

Education

$187K

Transportation

$942K

Construction

$3.01M

Education

$201K

Hospitality

$5M+

Retail

$1.92M

Transportation

$1.21M

Construction

$731K

Restaurant

$897K

Hospitality

$3M+

Education

$133K

Construction

$738K

Restaurant

$581K

Manufacturer

$2.82M

Healthcare

$3.6M

Healthcare

$578K

Healthcare

$1.07M

Farming

$926K

Retail

$2.82M

Construction

$187K

Hospitality

$3M+

Retail

$3.6M

Education

$187K

Transportation

$942K

Construction

$3.01M

Education

$201K

Hospitality

$5M+

Retail

$1.92M

Transportation

$1.21M

Construction

$731K

Restaurant

$897K

Hospitality

$3M+

Education

$133K

Construction

$738K

Restaurant

$581K

Manufacturer

$2.82M

Healthcare

$3.6M

Healthcare

$578K

Healthcare

$1.07M

Farming

$926K

Retail

$2.82M

Construction

$187K

Education

$1.9M

Restaurant

$1.55M

Service

$927K

Staffing

$1.15M

Construction

$1.31M

Healthcare

$7M+

Education

$3.6M

Construction

$187K

Construction

$1.05M

Construction

$521K

Hospitality

$5M+

Hospitality

$7M+

Hospitality

$10M+

Engineering

$2.22M

Construction

$3.49M

Restaurant

$4.66M

Non-profit

$1.34M

Hospitality

$5M+

Hospitality

$10M+

Education

$1.9M

Restaurant

$1.55M

Service

$927K

Staffing

$1.15M

Construction

$1.31M

Healthcare

$7M+

Education

$3.6M

Construction

$187K

Construction

$1.05M

Construction

$521K

Hospitality

$5M+

Hospitality

$7M+

Hospitality

$10M+

Engineering

$2.22M

Construction

$3.49M

Restaurant

$4.66M

Non-profit

$1.34M

Hospitality

$5M+

Hospitality

$10M+

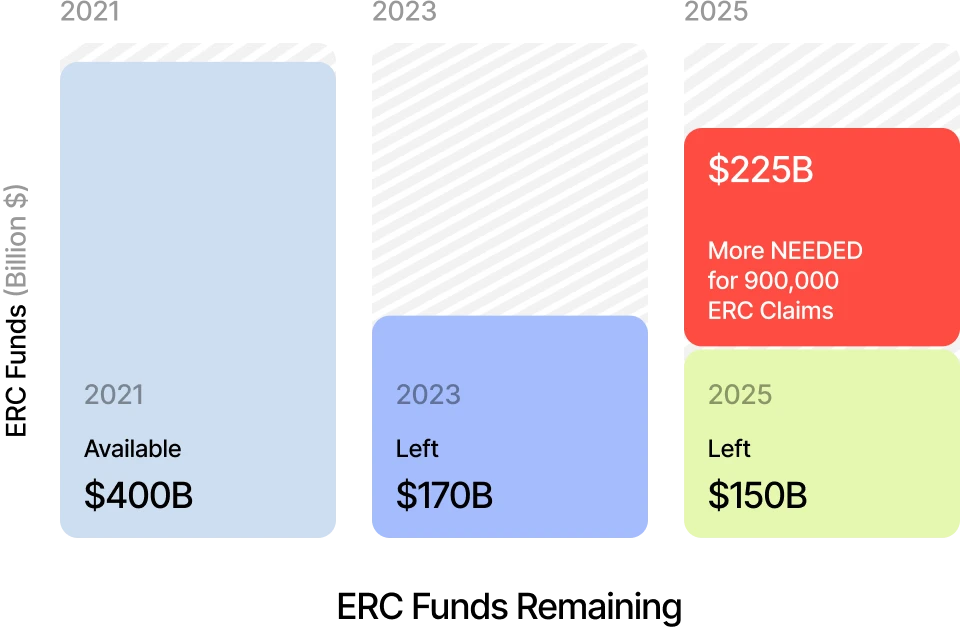

Over 60% of Claims Simply Won’t Be Paid – Will Yours?

1.5 Million ERC Claims = $375 Billion in Backlog

But Only $150 Billion is Left to Pay Them

$225 Billion Gap = 60% Won't Be Paid

60% Won’t Be Paid!

First Come,

First Serve!

100% Guaranteed

And it’s only getting worse…

20,000 new ERC claims are being filed every week—adding to the massive backlog.

The backlog is growing as newer filers expedite, pushing you further back in line.

If you don’t act now, your refund could disappear forever—either due to lack of funds or your claim expiring when the statute of limitations runs out.

Waiting Could Cost You Everything…

Only 40% of ERC claims will be paid before funds run out—there’s simply not enough money for everyone.

Your ERC claim could expire—The IRS is running out the statute of limitations clock on businesses.

Congress could cancel ERC at any time—leaving you with nothing and no chance of appeal.

The IRS backlog is growing —20,000 new ERC claims are being filed every week. Many are expediting and jumping ahead of you.

Unfortunately, it’s first come, first served— Will You Secure Your Refund or Risk Losing It?

Those who expedite their claims move to the front of the line.

Those who wait risk getting nothing at all.

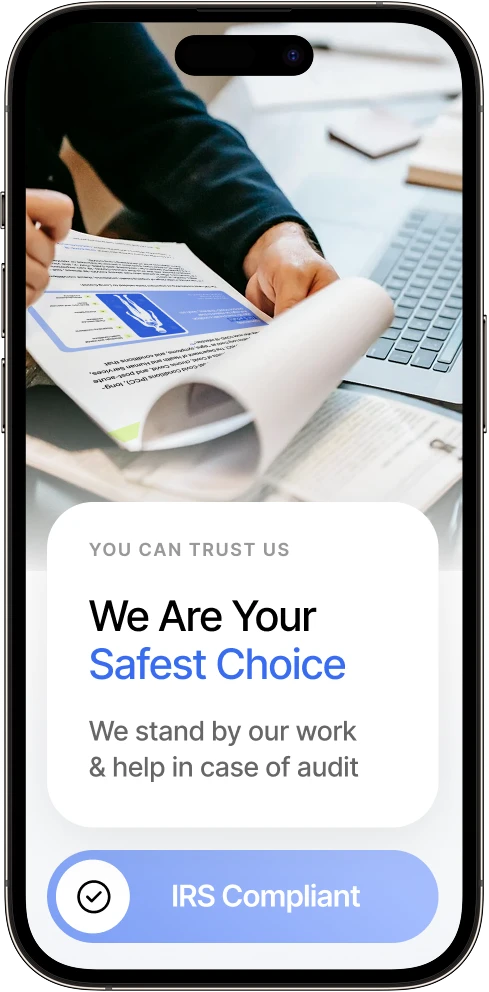

Audit Protection

100% Guaranteed

Some firms recommend suing the IRS, but that could cost you more money, more time, and create bigger problems.

Taking the IRS to court over your ERC refund could:

A lawsuit isn’t the answer if you want to avoid audits, legal risks, and costly delays.

The smartest, safest, and fastest way to get your ERC refund is our proven method—a friendly, lawsuit-free approach that works with the IRS, not against it.

Through expert-prepared, undeniable documentation, we compel the IRS to act—without legal battles, unnecessary risks, or years of waiting.

Expedite Your ERC Claim the Right Way—Without Suing, Without Stress, and Without Upfront Costs!

(01)

Move ![]() to the Front of the Line & Get Your Money Fast

to the Front of the Line & Get Your Money Fast

Secure Your Place Among the 40%Of Successful ERC Claims Left

Our ERC expedited process acts like a queue jump, pushing your claim to the front of the line so you can get paid in just 60-120 days instead of years.

ERC Expedited Report

A powerful legal report that compels the IRS to act immediately on your claim.

ERC Qualification Report

Full documentation confirming your eligibility, including stamped government orders that the IRS accepts.

![]() SCROLL

SCROLL

Step 1

We Build Airtight Documentation

Our legal and tax experts audit and strengthen your claim with airtight documentation, eliminating IRS red flags and preventing delays—ensuring fast-track approval.

100% Guaranteed

Step 2

We Advocate For You Directly With The IRS

We advocate directly with IRS liaisons, agents, and case managers to prioritize your claim.

Our legal team submits a powerful, 100+ page ERC Expedited Report that compels the IRS to act immediately.

We don’t just submit paperwork—we prove why your claim must be processed immediately. Our report highlights how the IRS has violated its own agency policies, Treasury regulations, and federal case law—demonstrating the unnecessary hardship businesses like yours have endured due to the IRS’s inaction.

Step 3

You Get Priority Processing & Your Checks — Fast!

Supported by our robust reports, your claim moves to the front of the line for IRS review. A dedicated IRS agent is assigned to your case, reviewing your claim with everything they need upfront—no back-and-forth, no delays.

![]() Now, all that’s left to do is check your mail—your ERC refund is on its way!

Now, all that’s left to do is check your mail—your ERC refund is on its way!

We Protect YOU

IRSplus is the #1

Other Firms Filed Your Claim—We Actually Get You Paid

Many ERC firms filed your claim and left you waiting , unable to speed up the process. Some even charge upfront fees or push risky lawsuits against the IRS, leaving businesses stuck with exorbitant legal fees and potential audits.

At IRSplus, we play smart— working directly with the IRS to move your claim to the front of the line.

For the past 8 years, we’ve been leading the way in tax credit solutions, building powerful relationships that allow us to offer the only real solution to the ERC backlog.

While most businesses are stuck waiting indefinitely, our clients receive their refunds in just 60-120 days.

That’s why thousands of businesses trust IRSplus to get their ERC refunds expedited when no one else can.

ERC Expedited Report: Get the IRS to Act Now

A powerful legal report that compels the IRS to prioritize and approve your claim—fast.

01

ERC Qualification Report: Ironclad Proof of Eligibility

Complete documentation, including stamped government orders, to eliminate delays and ensure approval.

02

Direct IRS Liaison: Skip the Backlog & Move to the Front

We cut through red tape with direct IRS advocacy and undeniable supporting evidence, ensuring priority processing of your claim.

03

100% Success Rate: Businesses Like Yours Are Already Getting Paid

Thousands of businesses have successfully expedited their ERC refunds with our proven process.

04

Why shouldn’t yours be next?

Future

IRSplus Expediting

Waiting in the IRS Backlog

Lawsuits Against IRS

Timeframe to Get Paid

![]() 60-120 Days

60-120 Days

![]() 2-3+ YearsIf any money is left

2-3+ YearsIf any money is left

![]() 2-3+ YearsIf any money is left

2-3+ YearsIf any money is left

Upfront Cost

![]() $0

$0

![]() $0 - $20,000

$0 - $20,000

![]() $50,000+

$50,000+

Application Process for Expediting

![]() Just 15 Minute

Just 15 Minute

![]() No Fast-Track option

No Fast-Track option

![]() 100s of Hours

100s of Hours

Lawsuit Needed?

![]() No

No

![]() No

No

![]() Yes

Yes

Legal Expedited Report

![]() Included

Included

![]() No

No

![]() No

No

Stamped Government Orders

![]() Included

Included

![]() No

No

![]() No

No

Audit Protection

![]() Included

Included

![]() No

No

![]() No

No

100% Risk-Free

![]() Yes

Yes

![]() No

No

![]() No

No

Customer Support

![]() 24/7 phone & text support

24/7 phone & text support

![]() None

None

![]() Expensive Hourly Billing

Expensive Hourly Billing

That’s right — with IRSplus there are

100% Risk-Free Guarantee

You only pay when you get paid!

No Upfront Fees

No hidden costs, no surprises.

No Lawsuits Required

We work with the IRS, not against them

Fastest ERC Processing Available

Get paid in 60-120 days, not years.

Direct IRS Liaison

Your claim is assigned to an IRS agent for priority review.

Trusted by Thousands of Businesses

We’ve successfully expedited countless ERC refunds.

Expedited Legal Report

Our ERC Expedited Report compels the IRS to act.

Documentation the IRS Loves

Ironclad proof ensures faster approval & fewer delays.

24/7 Support From Real Experts

Our team is available anytime to help you.

The IRS knows the ERC fund is running out, and as thousands of businesses expedite their claims, those who wait are falling further behind in the queue.

Over 60% of ERC claims will be denied or delayed past expiration—leaving over 900,000 business owners without the ERC refunds they’re owed.

But those who expedite NOW are receiving their checks in just 60-120 days!

Get Your Money Now – Expedite Your ERC Refund Today! Join Thousands of Business Owners Who Have Already Expedited Their ERC Refunds!

We Protect YOU

Expedite your claim

Compliance & Qualifications: Claim Your ERC with Confidence: Get Official Proof

Verify Your Eligibility with Official Government Orders

IRSplus strives to exceed the required compliance structure outlined by the IRS for ERC processing. We are one of the very few tax firms to provide clients with a stamped copy of all applicable government orders in the IRS acceptable format. Feel secure knowing your ERC claim and compliance is based on official government orders that proves your ERC eligibility. Get the peace of mind you deserve – see which orders apply to your business today

We’ve made it easy for you to see your preliminary Qualification Periods below! Although the PDF for your State pops up with limited view, there will be hundreds of pages that will be attached to your comprehensive report once you file your ERC with us.

File with us to receive your applicable government orders as part of our comprehensive ERC report

Stop Wondering if you Qualify

Get official government orders for 100% certainty

Alabama

Alabama

Select your State for your Preliminary Qualification Periods

Preliminary Qualification Period

03/13/2020-07/06/2021

45 Government Orders

File with us to receive your applicable government orders as part of our comprehensive ERC report

Our Features

You will never have to pay for a mistake WE make, GUARANTEED! Our ERC work is 100% insured AND we give it to you in writing!

Our clients have real people responding to them when needed. We are fast, efficient, and highly responsive. The ERC Specialist assigned to you ensures accurate qualification, calculations, and quick filing

About us

Team Expert

Our specialty financial and accounting tax firm is led by a team of passionate professionals who are committed to improving performance, results, and goals for our clients. We are dedicated to helping companies benefit from government incentive programs that are available to them.

Top Rated Tax Firm since 2017

Care about the success of our clients

However, we are much more than just a tax firm. We care about the success of our clients and strive to provide compassionate and honest service in everything we do.

We offer a complete spectrum of financial, tax and accounting, assurance and advisory services. Our industry-focused practices offer deep insight and specialized services to privately held and publicly registered companies, and nonprofit and social sector organizations. The Firm also provides a full complement of marketing, technology, wealth management, and virtual accounting staffing services.

Our mission

The more we care about your success, the more success we have too.

us in numbers

0+

Hours per month

0k

Cups of coffee a week

0

We are planting a tree and providing a meal for every ERC employee our clients have.

10,000,000+ Trees & Meals

ERC expediting is a service that moves your Employee Retention Credit (ERC) claim to the front of the IRS line, reducing your wait time from 2+ years to just 60–120 days.

✅ We don’t sue the IRS — we work with them.

IRSplus prepares an extensive legal ERC Expediting Report, which includes:

• ✅ Case law

• ✅ IRS procedural guidelines

• ✅ Statutory obligations

• ✅ Government orders

This legal-backed report is used to demonstrate urgency, support your eligibility, and compel the IRS to assign your claim to an agent for processing — something that’s not happening in the current backlog.

We work through IRS channels at both the federal and state levels to make this happen—without lawsuits or risky shortcuts.

Waiting puts your refund—and your business—at serious risk.

• ? IRS is still under a moratorium. Claims remain unassigned and unprocessed indefinitely.

• ? The IRS workforce has been cut by nearly 50%. Less staff = slower refunds.

• ? Only 40% of ERC claims are expected to be paid before the $150B in funds run out.

• ⏳ Your statute of limitations is expiring. Once it does, the IRS no longer has to pay you.

• ? Most ERC providers can’t expedite. Many were pop-up marketing firms with no IRS access.

• ✅ Expediting pushes your claim to the front—getting it assigned to an IRS agent and processed in 60–120 days instead of 2+ years.

• ?️ Your refund is legally supported. We build a 300+ page legal Expediting Report backed by case law and IRS policy to ensure your claim is heard.

Bottom line?

Expediting is the only proven way to speed up payment, reduce audit risk, and make sure your ERC refund actually arrives before it disappears.

Our expediting process is 100% legal and doesn’t involve suing the IRS.

We don’t use loopholes or adversarial tactics. Instead, we follow a technical, IRS-recognized process to escalate your claim—based on:

? There is a formal, technical process to demonstrate urgency to the IRS—one that must be supported by:

• ✅ Case law

• ✅ IRS procedural guidelines

• ✅ Statutory obligations

• ✅ Financial or operational hardship

Our legal team prepares a 300+ page ERC Expedited & Qualification Report tailored to your case that compels the IRS to assign and process your case—without litigation, delays, or conflict.

? Bottom line: We work with the IRS—not against them—to get you paid faster, without legal risk

Our proven 3-step process ensures your ERC claim is prioritized, approved, and paid—fast.

1. ERC Review & Intake

? You complete a simple intake form—takes just 10 minutes.

? We review your ERC qualifications for errors, red flags (even if it was filed by another firm).

? Our compliance team strengthens your claim and corrects any risks before submitting it to the IRS.

2. Legal Report & Advocacy

? We create a 300+ page ERC Expedited & Qualifications Report backed by federal tax code, case law, IRS procedures, and official government orders (500-900 pages).

? This report proves the urgency of your claim and legally compels the IRS to prioritize your file for immediate assignment.

? We include:

• ✔️ Case law requiring expedition

• ✔️ Statutory obligations the IRS must follow

• ✔️ Procedural IRS rules they’ve violated

• ✔️ Government orders that support your claim

? We don’t just submit paperwork—we make a legal case they can’t ignore.

3. IRS Escalation & Fast Approval

? Our tax attorneys and lobbyists escalate your claim directly to IRS decision-makers.

? Your file is flagged, assigned to an IRS agent, and reviewed faster than standard claims.

? Result: ERC refund paid in 60–120 days, not 2+ years.

? You keep your place in line—expediting never resets or delays your filing.

✅ All of our work is backed by Berkshire Hathaway E&O insurance, includes Audit Protection, and is 100% risk-free with no upfront cost.

No upfront fees. No risk. No surprises.

Our service is 100% success-based—you only pay after you receive your ERC refund.

? Our fee is a simple percentage of your refund, clearly outlined in your agreement with no hidden costs.

✅ If you don’t get paid, we don’t get paid.

✅ No retainers. No hourly billing. No legal fees.

✅ Just results—backed by a track record of thousands of expedited claims.

Expediting with IRSplus gets you paid in just 60–120 days.

By contrast, standard IRS processing is still taking 1–2+ years—with no clear timeline, no communication, and no guarantee you’ll even get paid.

And with ERC funds rapidly running out, waiting in the backlog isn’t just slow—it’s risky.

✅ Our clients are seeing results in weeks, not years—without lawsuits or upfront fees.

? Expediting is the only proven way to skip the IRS delays and secure your check.

No problem—this is actually very common.

We specialize in expediting ERC claims originally filed by other companies. In fact, most of our clients come to us after realizing their original provider has no ability to speed up the process.

? Here’s the truth:

Over 90% of ERC firms were pop-up companies created during the rush—often run by marketing agencies, mortgage brokers, or payroll resellers. They knew how to file, but not how to qualify clients properly, fix errors, or navigate the IRS to get refunds actually approved and paid.

These companies:

• ❌ Don’t have relationships with the IRS

• ❌ Don’t understand federal tax code

• ❌ Don’t offer audit protection or insurance

• ❌ Can’t legally expedite your claim

✅ At IRSplus, we review and strengthen your original filing, catch red flags that could delay or cancel your refund, and then build a legal case to get your claim prioritized.

Best of all?

Expediting your claim with us does not affect your place in line. You keep your original IRS filing date—we just get it moving.

We’re not just another ERC firm—we’re the firm others refer to when they can’t get the job done.

✅ No Upfront Fees — 100% Risk-Free

✅ We don’t sue the IRS — we work with them to get you paid faster

✅ Thousands of ERC claims expedited — with a 100% success rate

✅ All work is insured by Berkshire Hathaway E&O Insurance

✅ Handled in-house by expert tax attorneys & CPAs — never outsourced

For the past 8 years, IRSplus has secured billions in federal, state, and local tax credits for businesses across 51+ industries nationwide. We are a full-service tax compliance and advisory firm—not a pop-up ERC vendor.

Our services include:

• Tax credit specialization (ERC, SETC, WOTC, and more)

• Advisory & strategic planning

• Audit & wealth management services

As a no-risk firm, you only pay after you receive your ERC. And with our insurance-backed guarantee and 100% compliance history, your refund—and your peace of mind—are fully protected.

No—and here’s why:

Most CPAs and payroll providers don’t have the IRS legal pathways, documentation, or experience required to expedite ERC claims. They may have filed your ERC—but filing is the easy part. Expediting requires much more.

They usually lack:

• ✅ Access to government orders

• ✅ Legal expertise to justify urgent processing

• ✅ Audit protection and insurance-backed guarantees

• ✅ IRS advocacy channels to escalate your claim

In fact, many of these filings are flawed or incomplete—and could actually delay or jeopardize your refund. That’s why we review and strengthen your original claim before we expedite it.

As for other ERC expeditors: Most rely on lawsuits to pressure the IRS—an expensive, time-consuming, and risky approach.

? IRSplus is likely the only firm in the country successfully expediting ERC claims without suing the IRS. Our method is legal, fast, and fully backed by expert compliance.

Yes—by far. It’s faster, safer, and doesn’t cost you $50,000 upfront.

Litigation can take years, involve extensive legal battles, and typically requires a minimum ERC claim of $1 million or more just to be considered by law firms. Many attorneys charge $50,000+ upfront retainers to even begin the process—and there’s no guarantee of success.

At IRSplus, we take a different approach.

✅ We don’t sue the IRS—we work with them.

✅ We’ve built a direct IRS advocacy process that compels them to prioritize your claim through legal reports, statutory rules, and federal case law—without going to court.

✅ We accept all clients, big and small. Whether your ERC is $30,000 or $3 million, your claim deserves to be expedited.

Best of all, our service is:

• ✅ No upfront fee

• ✅ Fully insured

• ✅ 100% risk-free

You don’t need a courtroom to get your refund—you need IRSplus.

You don’t need a courtroom to get your refund—you need IRSplus.

No worries—nothing is lost, and you owe us nothing.

Before we begin, our legal and tax team conducts a thorough review of your file to determine if your ERC claim meets the IRS’s criteria for expedited processing.

? The good news? More than 85% of applicants do qualify.

But if your case doesn’t meet the necessary standards:

• ✅ We’ll let you know upfront

• ✅ Your ERC filing remains fully active with the IRS

• ✅ Your agreement is canceled

• ✅ You’re never charged a dime

No risk. No delay. No downside.

We only move forward with clients when we’re confident we can help—and if we do, it’s because we believe we can get you paid faster.

We can still help.

IRSplus works with businesses that filed through PEOs (Professional Employer Organizations). We coordinate with your PEO to gather required documentation and ensure your expedite request is fully supported.

For Business Owners

The IRS is still delayed. Your refund isn’t coming unless you push it forward. We’ll get it done — fast, legal, and guaranteed

Secure your spot before ERC funds run out.

888-210-8870Expedite your ERC today

100% Risk-Free

![]() Our ERC work is Insured AND we give it to you in writing!

Our ERC work is Insured AND we give it to you in writing!